We guarantee to show you how to save thousands of dollars and pay off your home in one third of the time.

IF WE DON'T DELIVER... YOU PAY NOTHING!

In fact, the first 18.5 years of a traditional mortgage doesn't really inspire much hope because most of the payments you make go towards interest.

Making mortgage payments and not seeing the balance go down is frustrating. (Thanks, Captain Obvious.)

What's even more frustrating is if you don't have tons of extra money to put towards the mortgage, it isn't in any hurry to go away either.

The thing is, over in Australia and Great Britain, this is the NORM. Homeowners with mortgages are the minority.

The biggest reason this isn't as popular over in the United States is because think about how many trillions of dollars banks would lose in interest if they started promoting a HELOC over a mortgage. They ALL have HELOCs, they just don't promote them.

Want to know what the banks are doing? They want you to put a little money in your checking, a little money in your savings and maybe some in a money market. It's called segregation of income.

Plus, they only offer you closed end mortgages so this way you don't put all of your money into your mortgage each month because you can't get it back out.

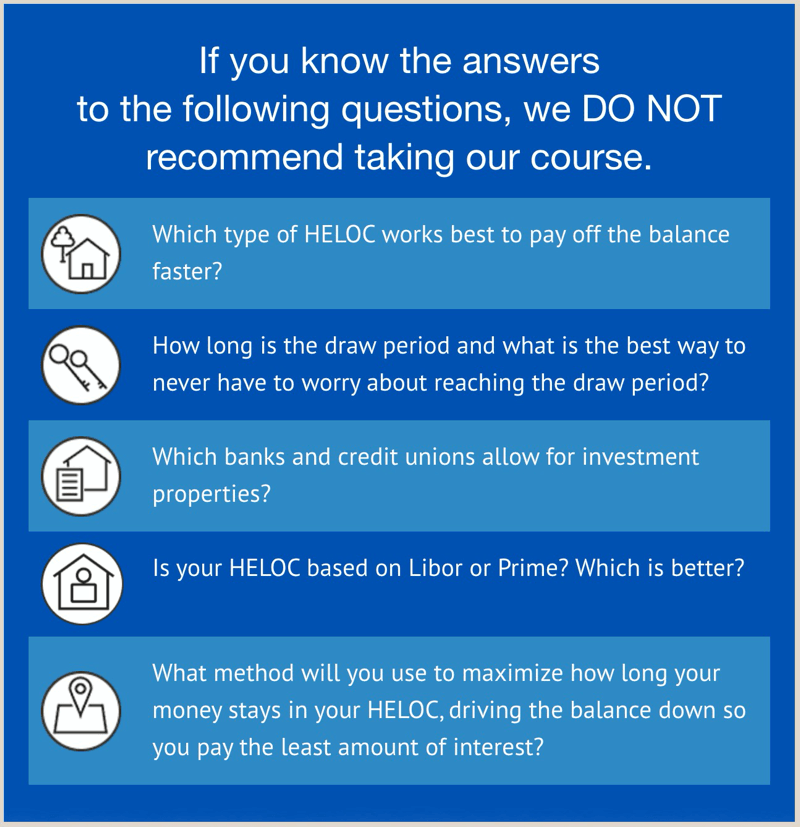

Ask yourself, Did they even offer you the chance to get a HELOC instead of a mortgage on your last home - although it’s financially better for you?

You can take the online course right from the comfort of your home, anytime, and as many times as you like. You will work directly with Michael Lush as he guides you through the process.

You will get a list of banks and credit unions that offer the HELOC based on your state. You want to know which banks offer 80, 90 and even 100% financing? We have that list which took hundreds of hours of research. You want to know which bank or credit union to apply to for investment properties? No problem. We have several.

While saving tens of thousands of dollars alone is worth it, we go deeper by teaching you how to use the HELOC to build wealth. It's true. You will not only be saving money but learning how to make it as well. The class covers six topics over the course of three individual classes.

We want you to take action and replace your mortgage as fast as possible so you can start saving right away. But there is something else that is unique about us.

You could hunt for the right loan and bank for yourself like Michael did when he started this journey with his family. Just be prepared to end up on page 17 of Google when searching for banks and their guidelines.

Got questions during your search? Hopefully you will find a loan officer that is educated enough about this method who can answer them for you.

With enough Googling, you could eventually find out how to use the cash flow strategy that we teach. You see, getting a HELOC is only a tool. It is knowing how to use it that makes it so powerful.